Abstract

The advent of the digital age has reshaped the processes by which

data are collected, shared, and analyzed. An important trend within this

landscape is the integration of disparate data sources, often collected

independently and stored in isolation. Consequently, methods for data

integration are needed to realize the value of all existing data sources

in combination. Among these methods, Record Linkage (RL) plays a pivotal

role by enabling the connection of individual records across multiple

data sets. RL spans a wide array of contemporary applications, including

the linkage of survey data, administrative and electronic health

records, as well as historical censuses and vital records. Open-source

software to facilitate RL when records are linked using

quasi-identifiers is widely available. However, software for analyzing

linked files that accounts for the uncertainty and error-prone nature of

RL is lacking. Specifically, there is lack of software in the secondary

analysis setting in which RL and downstream analysis are conducted

separately. We describe postlink, an R package dedicated to

analyzing data integrated using error-prone record linkage. A central

feature of the package is its extensible, formula-based architecture,

offering a suite of post-linkage counterparts to R’s standard modeling

toolkit.

1. Introduction

Information integration across multiple data sources is increasingly being applied in various scientific and policy contexts. Record linkage (RL) and privacy preserving record linkage (PPRL) refer to a set of tools that identify records on the same entity across data sources. In the absence of unique identifying information, RL and PPRL are prone to errors. Records from different entities may be incorrectly linked (false matches), and records that correspond to the same entity may be missed (false non-matches). These errors can result in biased and inaccurate estimates (Neter et al., 1965). To obtain statistically valid estimates, analyses of linked datasets should adjust for these errors (Chambers & Diniz da Silva, 2020; Kamat & Gutman, 2026; Wang et al., 2022). However, because of privacy considerations, the original datasets and the information pertinent to adjustment may be limited or absent. This challenge is referred to as secondary analysis, in which the linkage is performed by one organization and the analyses of the linked data-sets are implemented by other organizations. The National Institute on Aging (NIA) LINKAGE project, which enables access to NIA-funded study data linked to administrative records from the Centers for Medicare & Medicaid Services, is a prominent example of such a setting (National Institute of Aging, 2025). We use the term post-linkage data analysis (PLDA) to describe statistical analyses of data that have been generated through record linkage or privacy preserving record linkage.

Multiple R packages have been developed to link records in the

absence of unique identifiers. Some of these applications are based on

the Fellegi-Sunter model (Fellegi & Sunter, 1969),

RecordLinkage (Sariyar & Borg, 2025),

fastLink (Enamorado et al., 2023). More recently,

Bayesian record linkage packages were developed, bstrl

(Betancourt et al.,

2022), BRL (Sadinle, 2017) and blink

(Steorts, 2020).

In addition, privacy preserving record linkage package is available

through PPRL (Schmiedel, 2025). Python record linkage

tools such as Splink (Linacre et al., 2022),

recordlinkage (De Bruin, 2019),

dedupe (Gregg

& Eder, 2022), gfs_sampler (Farley & Gutman,

2020), and anonlink (Data61, 2017) have been developed to

offer flexible and scalable linkage solutions.

After the linkage process is complete, it is imperative to evaluate

the quality of the linkage and address possible linkage errors in

downstream analysis. The ER-Evaluation package in Python

(Binette &

Reiter, 2023) has been developed to assess linkage quality

using benchmark data. However, dedicated tools to conduct statistical

analyses that account for potential linkage errors are absent. A common

statistical tool to estimate the relationship between an outcome and a

set of covariates are linear and generalized linear models. These models

are efficiently implemented with the lm() and

glm() commands in R (R Core Team, 2024). Applying these methods

directly to linked datasets assumes that all records are correctly

linked, with no erroneous matches. Although statistical methods to

adjust for linkage errors have been proposed (Kamat & Gutman, 2026), the

corresponding software is often not readily accessible. This poses a

barrier to the adoption and application of these methods in practice.

(Chambers,

2009) provides R functions to adjust for linkage errors

within the regression framework. These methods assume that the

probability of a mismatch is constant across records within defined

subgroups (i.e., exchangeable linkage errors). However, the available R

functions are largely limited to estimating equations for linear and

logistic regressions, and are geared toward simulation and

methodological illustration. As such, they are not well suited for

routine use by analysts or subject-matter experts and may be

computationally inefficient.

We have developed an R package, postlink (Bukke et al.,

2026), that provides a cohesive and user-friendly

implementation of PLDA methods across a range of settings and input

types. The package is available from the Comprehensive R Archive Network

(CRAN) at https://CRAN.R-project.org/package=postlink, and is

implemented using a common modeling interface while adjusting for

falsely linked records. The postlink package focuses on

methods for secondary analysis. In primary analysis settings, where

individual files are accessible, methods that jointly perform record

linkage and analysis with direct propagation of uncertainty are more

appropriate.

The postlink R package consolidates three foundational

frameworks for post-linkage data analysis. First, the software

implements expectation-maximization (EM) based mixture modeling, which

absorbs the precursor package pldamixture (Bukke et al.,

2024) and facilitates contingency table analysis based on

methods developed in Slawski et al. (2025). Second, the package

incorporates a Bayesian mixture modeling approach proposed in Gutman et al. (2016). This approach enables the

estimation of model parameters after adjustments for linkage errors, as

well as using multiple imputations of the latent match status (correctly

vs. incorrectly linked records). The imputed match status can then be

used to fit post-linkage models not originally specified, using standard

multiple imputation combining rules (Rubin, 1996). Third, the package

integrates bias-adjusted estimating equations following the work of

Chambers (2009) for generalized

linear models and Vo et al. (2024) for Cox proportional hazards

regression. Within postlink, the methods in Chambers (2009) are extended to

encompass the Poisson and Gamma regression models. In addition, our

implementation improves the scalability of these methods for larger

datasets and their accessibility for analysts.

Subsequent sections of the paper are structured as follows. Section 2 provides an overview of the

postlink package. Section 3

details the three adjustment methods implemented in the R package. Section 4 illustrates the usage of the

package with a case study. We conclude and discuss future directions in

Section 5. Further demonstrations and details

regarding the package functionality are available on the

postlink website at https://postlink-group.github.io/postlink/. The

long-term goal of postlink is to progressively expand its

functionality to support a broad range of linkage and post-linkage

analysis scenarios.

2. The postlink Architecture

The postlink package provides an extensible

computational framework for post-linkage data analysis (PLDA). Given the

diversity in record linkage pipelines—both in underlying data structures

and in the amount of linkage information available—the software is built

using a modular, object-oriented R architecture. As illustrated in

Figure 1, the workflow leverages S3 method dispatch to decouple the

specification of linkage uncertainty from the substantive statistical

modeling. This separation serves three primary software design

objectives: (1) providing a unified interface for diverse post-linkage

scenarios; (2) allowing practitioners to propagate linkage uncertainty

using standard regression paradigms; and (3) separating the internal

mechanics of the package from its public application programming

interface (API) to facilitate extensibility.

The user workflow is consequently partitioned into two phases: 1) Adjustment Specification and 2) Estimation & Inference. In the first phase, the focus is on formulating the nature of the data and the linkage errors. The second phase focuses on the scientific questions that need to be addressed using the data.

Figure 1: Schematic of the typical two-phase

postlink workflow, illustrating the decoupling of the

adjustment specification from the outcome model fitting.

Phase 1: Adjustment Specification

In the first phase, the analyst defines the linked dataset and the

available information about the linkage process using a constructor

function. These functions, prefixed with adj, correspond to

different frameworks (e.g., weighting-based methods or mixture modeling

approaches). Section 3 describes the specific

adjustment methods and linkage error scenarios currently supported. The

constructors perform an initial validation layer to check for coherence

between the data structure and the assumptions of the chosen adjustment

methodology. Upon successful validation, the constructor returns a

structured S3 Adjustment object. To accommodate large-scale

data, this object is engineered as a lightweight container. This

construction minimizes memory overhead by retaining essential metadata

and accessing the underlying data by reference to avoid duplication. The

Adjustment object also implements context-specific methods

for standard generics (e.g., print(), plot()),

enabling diagnostic inspection of the linkage assumptions before model

fitting.

Phase 2: Estimation and Inference

The second phase handles model fitting through a suite of wrapper

functions designed to mirror standard R regression interfaces. The

current core functions include plglm() for generalized

linear models, plcoxph() for Cox proportional hazards,

plsurvreg() for parametric survival models, and

plctable() for contingency table analyses. Using S3

dispatch, these wrappers automatically retrieve the encapsulated

specifications from the provided Adjustment object and

perform the corresponding internal inference routine. This design allows

analysts to use the familiar formula-based syntax of core R functions

(e.g., stats::glm(), survival::coxph()), while

the package manages the underlying computational complexity. The

resulting fitted model objects integrate with the R ecosystem,

supporting standard post-modeling generics such as

summary(), confint(), vcov(), and

predict(). For Bayesian adjustments, multiple imputation

pooling is supported with a generic mi_with() function.

Dual-Access Interface

Complementing the two-phase workflow, the underlying computational

routines are also available (e.g., glmELE(),

coxphMixture(), survregMixBayes()). The S3

framework can be bypassed to invoke these routines directly, a

capability advantageous for performance-critical tasks, such as

large-scale simulation studies, or for developers prototyping new

adjustment algorithms. This decoupling also ensures that emerging PLDA

methodologies can be integrated without altering the established

modeling syntax.

3. Adjustment Methods for Secondary Analysis

We describe the theoretical foundation for the secondary analysis

methods that are supported in postlink. We assume that the

linked dataset, denoted as LD,

comprises of n record pairs. For entity

i \in \{1, \dots, n\}, we observe a

single outcome variable Y_{Ai} and a

set of covariates \mathbf{X}_{Ai}

originally recorded in data source A, alongside a set of covariates

\mathbf{X}_{Bi} originally recorded in

data source B. Formally, the linked data is defined as LD = \left(\mathbf{X}_{B}, \mathbf{Y}_A,

\mathbf{X}_A \right), where \mathbf{X}_{B} =

\{\mathbf{X}_{B1},\ldots,\mathbf{X}_{Bn}\}, \mathbf{Y}_{A} = \{Y_{A1},\ldots,Y_{An}\} and

\mathbf{X}_{A} =

\{\mathbf{X}_{A1},\ldots,\mathbf{X}_{An}\}. Suppose that an

analyst utilizes dataset LD to estimate

the conditional distribution p(Y_{Ai} \mid

\mathbf{X}_{Ai},\mathbf{X}_{Bi};\boldsymbol{\beta}), where \boldsymbol{\beta} is a set of unknown

parameters governing this distribution. Because LD is formed by merging two separate data

sources without unique identifiers, it contains the observed paired

outcome Y_{Ai}^*, which may differ from

the true outcome Y_{Ai} because of

linkage errors (Y_{Ai}^* \neq Y_{Ai}).

As a result, LD includes both true and

false links, and only limited information on overall linkage quality may

be available (e.g., estimated mismatch rates within blocks).

When the original data sources are of the same size and they both represent the same entities, the observed vector \mathbf{Y}_{A}^* is a permuted version of true vector \mathbf{Y}_{A}, such that \mathbf{Y}_{A}^* = \Delta\mathbf{Y}_{A}, where \Delta is an n\times n permutation matrix with exactly one entry equal to one in each row and column. When there are no errors in the linkage, \Delta is the identity matrix and \mathbf{Y}_{A}^*=\mathbf{Y}_{A}.

This notation cannot be utilized when the dataset includes some records that represent the same entities, and some records that do not. To address this limitation, we rely on an indicator variable C_i with C_i=1 for correct matches, i.e., Y_{Ai}^*=Y_{Ai}, and C_i=0 otherwise, 1 \leq i \leq n.

A naive estimator \widehat{\boldsymbol{\beta}}_N of the

parameter \boldsymbol{\beta} is

obtained by regressing \mathbf{Y}_A^*

on \mathbf{X} = [\mathbf{X}_A \;

\mathbf{X}_B]. This estimator is typically biased when \mathbf{Y}^*_{A} \neq \mathbf{Y}_{A} (Kamat & Gutman,

2026; Neter et al., 1965; Wang et al., 2022). To mitigate this

bias, postlink provides three distinct adjustment

frameworks, which are accessible through the package’s two-phase

adj*() and pl*() architecture. Table 1

provides an overview of these frameworks, their constructor functions,

and statistical modeling they currently support.

Table 1: An overview of three PLDA frameworks implemented in

postlink

| Framework | Constructor | Primary Use Case | Supported Models |

|---|---|---|---|

| Weighting | adjELE() |

When block-level mismatch rates are given (e.g., from audit samples). | GLMs, CoxPH |

| Mixture Modeling | adjMixture() |

When continuous or categorical paradata on linkage quality (e.g., string distances) are available. | GLMs, CoxPH, Contingency Tables |

| Bayesian Mixture | adjMixBayes() |

When exploring multiple scientific models or to incorporate prior knowledge. | GLM, Parametric Survival |

3.1 Weighting

The first approach relies on weighting the estimating equations to correct for mismatch bias. Suppose that \mathbf{X} = \mathbf{X}_B, so that there are no covariates residing with the outcome in data source A. In addition, dataset LD is partitioned into Q blocks, where block q \in \{1,\dots, Q\} is of size n_q, and n = \sum_{q=1}^{Q} n_q. Block partitioning is commonly used to reduce the computational complexity of linkage algorithms. Blocks are formed by requiring exact agreement on categorical linking variables across datasets, such that all individuals within a block share the same values on these variables. Let \mathbf{Y}^{*}_{Aq}, \mathbf{X}_{Bq} and \Delta_q denote the response variable, the matrix of covariates, and a binary matrix of order n_q in block q, respectively. Under the non-informative linkage assumption (Chambers, 2009; Kamat & Gutman, 2026), \Delta_q is independent of \mathbf{Y}_{Aq} given \mathbf{X}_{Bq}, which implies that E(\mathbf{Y}_{Aq}^* \mid \mathbf{X}_{Bq}) = E(\Delta_q \mid \mathbf{X}_{Bq}) E(\mathbf{Y}_{Aq} \mid \mathbf{X}_{Bq}) = E_q f_q(\boldsymbol{\beta}), where E_q = E(\Delta_q \mid \mathbf{X}_{Bq}), and f_q(\boldsymbol{\beta}) = E(\mathbf{Y}_{Aq} \mid \mathbf{X}_{Bq}) is the regression function under correctly linked data. When the data is correctly linked, an estimating equation for \boldsymbol{\beta} is of the form \sum_{q=1}^{Q} \mathbf{G}_q(\mathbf{X}_{Bq}, \boldsymbol{\beta}) \left\{\mathbf{Y}_{Aq}-f_q(\boldsymbol{\beta}) \right\}=0, where \mathbf{G}_q(\mathbf{X}_{Bq}, \boldsymbol{\beta}) is a weighting matrix that is independent of \mathbf{Y}_{Aq}. However, we only have access to \mathbf{Y}^*_{Aq}. Replacing \mathbf{Y}_{Aq} with \mathbf{Y}^*_{Aq} results in the naive estimator \widehat{\boldsymbol{\beta}}_N. This estimator is biased when some of the units are incorrectly linked (Chambers, 2009). To correct for the bias in \widehat{\boldsymbol{\beta}}_N, we modify the equation to adjust for linkage errors, \sum_{q} \mathbf{G}_q(\mathbf{X}_{Bq}, \boldsymbol{\beta}) \left\{ \mathbf{Y}^*_{Aq} - E_q f_q(\boldsymbol{\beta}) \right\} = 0. Chambers (2009) constructed E_q under the exchangeable linkage error (ELE) model [E_q]_{ij} = \begin{cases} \lambda_q, & \text{if record pair } (i,j) \text{ is a link},\\ \frac{1 - \lambda_q}{n_q - 1}, & \text{otherwise}, \end{cases} where \lambda_q is the proportion of correct links in block q, and it is either known to the analyst or estimated from audit samples.

The choice of \mathbf{G}_q(\mathbf{X}_{Bq}, \boldsymbol{\beta}) leads to different estimators. For example, in linear regression, \mathbf{G}_q = \mathbf{X}_{Bq}^\top yields a ratio-type adjustment estimator, which is similar to the one proposed by Scheuren & Winkler (1993). Setting \mathbf{G}_q = \mathbf{X}_{Bq}^\top E_q results in the estimator proposed by Lahiri & Larsen (2005). Setting \mathbf{G}_q = \mathbf{X}_{Bq}^\top E_q^\top (\boldsymbol{\Sigma}_q + \mathbf{V}_q)^{-1} leads to the best linear unbiased estimator (BLUE) of \boldsymbol{\beta}, where \mathbf{V}_q = \mathrm{Var}(\Delta_q E(\mathbf{Y}_q \mid \mathbf{X}_{Bq}) \mid \mathbf{X}_{Bq}) and \boldsymbol{\Sigma}_q is a diagonal matrix containing the observation-specific error variances, \sigma_i^2 = \mathrm{Var}(Y_i \mid \mathbf{X}_{Bi}), 1 \leq i \leq n. Because the BLUE depends on unknown quantities, it can be approximated using an iterative procedure in which these quantities are replaced by successively refined estimates.

This suite of weighting methods has been extended to generalized linear models (Chambers, 2009) and time-to-event models (Vo et al., 2024). Corresponding sandwich-type variance estimators have also been derived (Chambers, 2009).

In postlink, this procedure is implemented using the

two-phase workflow. First, the analyst specifies the ELE assumptions

using the adjELE() constructor:

adjELE(

linked.data,

m.rate, # Block-specific or global mismatch rates

audit.size, # Optional: Sample sizes for clerical review audit

blocks, # Vector defining the blocking structure

weight.matrix # Specifies the G_q matrix formulation

)The m.rate argument supplies block-specific or global

probabilities of mismatch, 1-\lambda_q.

The blocks argument is an indicator for the blocking

structure, which can be omitted if no blocks are present. If the

mismatch rates are estimated from a clerical review, the

audit.size argument can be supplied to accordingly inflate

the variance estimation. The form of the weighting matrix can be

specified in weight.matrix, allowing the user to select

between the ratio-type adjustment ("ratio"), the

Lahiri-Larsen estimator ("LL"), the best linear unbiased

estimator ("BLUE"), or "all" to compute all of

them simultaneously.

Once the adjustment object is validated and constructed, it is passed

to a standard modeling wrapper, such as plglm() for GLMs or

plcoxph() for survival analysis using Cox proportional

hazard model:

plglm(formula, family = "gaussian", adjustment, control, ...)

plcoxph(formula, adjustment, control, ...)The parameter formula describes the relationship between

\mathbf{Y}_q^* and \mathbf{X}_{Bq}, while the parameter

family describes the link function. These arguments

correspond to the regression mean function f_q(\boldsymbol{\beta}). The parameter

family is set to "gaussian" by default, but

can take the values "binomial", "poisson", or

"gamma". The control parameter allows the user

to specify starting values for the iterative algorithm used to estimate

\boldsymbol{\beta}. By default, the

naive estimator is used as the initial value for ratio-type and

Lahiri–Larsen weight matrix adjustments. For the BLUE weight matrix, the

Lahiri–Larsen estimator serves as the default starting value for

estimating \boldsymbol{\beta}.

The backend implementation differs from that of Chambers (2009) primarily in how the

expected estimating equation is handled. By relying on vectorized

operations for block-wise processing and analytically simplifying E_q M into a sum of column means and scalar

constants, the internal computational routine reduces the computational

complexity from \mathcal{O}(n_q^2 d)

down to \mathcal{O}(n_q d), where d represents the number of covariates in the

model (see Appendix A). The nleqslv package (Hasselman, 2023) is

used to solve the non-linear system of equations.

3.2 Inferring true links via latent mixture modeling (EM)

An alternative set of methods that adjusts for linking errors attempts to estimate the configuration of match status indicators \mathbf{C}= \{C_i\}. For record pair i, let \mathbf{Z}_i denote auxiliary variables available at the secondary analysis stage that may be associated with C_i. Following Gutman et al. (2016) and Slawski et al. (2025), a two-component mixture model for \mathbf{C} can be specified as \begin{align} Y_{Ai},\mathbf{X}_{Ai},\mathbf{X}_{Bi} \mid \mathbf{Z}_i,C_{i}=1 & \sim p_m(Y_{Ai},\mathbf{X}_{Ai},\mathbf{X}_{Bi} \mid \mathbf{Z}_i;\boldsymbol{\beta}_m), \\ Y_{Ai},\mathbf{X}_{Ai},\mathbf{X}_{Bi} \mid \mathbf{Z}_i,C_{i}=0 & \sim p_u(Y_{Ai},\mathbf{X}_{Ai},\mathbf{X}_i \mid \mathbf{Z}_i;\boldsymbol{\beta}_{u}), \\ C_i & \sim \text{ Bernoulli }(h(\mathbf{Z}_i;\boldsymbol{\xi})), \end{align} where \boldsymbol{\beta}_m and \boldsymbol{\beta}_u govern the joint distributions p_m and p_u of (Y_{Ai}, \mathbf{X}_{Ai},\mathbf{X}_{Bi}) among true links and false links, respectively. Moreover, h(\cdot\,;\boldsymbol{\xi}) denotes the conditional probability of a true link given \mathbf{Z}_i, with \boldsymbol{\xi} denoting the associated parameters. Slawski et al. (2025) do not consider \mathbf{X}_{Ai} co-occurring with the outcome in data source A and model p_m(Y_{Ai}, \mathbf{X}_{Bi} \mid \mathbf{Z}_i; \boldsymbol{\beta}_m) and p_u(Y_{Ai}, \mathbf{X}_{Bi} \mid \mathbf{Z}_i;\boldsymbol{\beta}_u). In addition, they assume that p_u(Y_{Ai}, \mathbf{X}_{Bi} \mid \mathbf{Z}_i;\boldsymbol{\beta}_u) = p_{uY}(Y_{Ai};\boldsymbol{\beta}_u) \cdot p_{u\mathbf{X}}(\mathbf{X}_{Bi} \mid \mathbf{Z}_i;\boldsymbol{\beta}_u), and estimate \boldsymbol{\beta}_m by maximizing the likelihood resulting from the mixture model using the EM algorithm (Dempster et al., 1977) while a plug-in estimator is used for p_u. The function h(\cdot\,;\boldsymbol{\xi}) can be parameterized in different ways. For instance, h(\cdot\,;\boldsymbol{\xi}) can be modeled according to a logistic regression model, with specific constraints on the linear predictors to facilitate estimation. An intercept-only specification of this logistic regression model corresponds to assuming a constant prior mismatch probability. Standard errors for the estimate of \boldsymbol{\beta}_m are computed using a normal approximation for the sampling distribution of the point estimator.

The EM-based mixture model requires specification using

adjMixture():

adjMixture(

linked.data,

m.formula, # Formula for the mismatch indicator model

m.rate, # Optional: global mismatch rate constraint

safe.matches # Optional: indicator for known true links

)The parameter m.formula takes a one-sided formula object

to model the conditional probability of a false link given the auxiliary

variables \mathbf{Z}_i, 1-h(\cdot\,;\boldsymbol{\xi}). The default is

an intercept-only model (~ 1), corresponding to a constant

marginal mismatch rate. The parameter m.rate allows the

user to supply an estimate to constrain the global mismatch rate. The

parameter safe.matches is a logical vector that indicates

records that are known to be correct matches, fixing their correct

linkage probability to 1 during the estimation process.

Because the adjustment specification is decoupled from the modeling

syntax, the same Adjustment object can be passed to

plglm(), plcoxph(), or plctable()

for analyses. For example, fitting an adjusted contingency table

requires only the formula and the adjustment object:

plctable(formula, adjustment, control, ...)The internal routine retrieves the S3 object, checks for coherence, and dispatches the customized EM algorithm, which iteratively updates the posterior probability that a record is a correct match in the E-step, and maximizes model parameters in the M-step.

3.3 Bayesian mixture modeling and multiple imputation

While the EM approach yields robust maximum likelihood estimates for

a specified p_m, researchers may also

wish to propagate linkage uncertainty into downstream analyses that are

not easily accommodated within an EM framework. In addition, analysts

may use complex models to identify erroneous links but report results

from a simpler primary analysis model. To support these settings,

postlink implements a Bayesian mixture model (Gutman et al.,

2016) for estimating the parameters. Note that in the

Bayesian formulation, \mathbf{X}_i

includes both \mathbf{X}_{Ai} and \mathbf{X}_{Bi}, and parameter constraints

can be imposed through the specification of prior distributions.

Posterior inference can be performed using the data augmentation procedure (Tanner & Wong, 1987), which alternates between imputing \mathbf{C} and updating the model parameters. When p_m coincides with the analysis model of interest, inference based on posterior draws of \boldsymbol{\beta}_m incorporates the uncertainty about \mathbf{C}. In settings where p_m differs from the analysis model, post-linkage inference can be obtained using multiple imputation (Rubin, 1987). Multiple imputed realizations of \mathbf{C} are drawn from the posterior distribution. Each realization is used to fit the analysis model separately, and resulting point and interval estimates are combined across imputations using standard multiple imputation combining rules (Little & Rubin, 2002; Rubin, 1996).

The underlying software for sampling from the posterior distribution

is based on Stan (Stan

Development Team, 2024) and the rstan package

(Stan Development Team,

2025), which employs the No-U-Turn Sampler to draw samples

from the posterior distribution of the parameters (Hoffman & Gelman,

2014). Given the kth draw of

the parameters \boldsymbol{\beta}^{(k)}_{m}, \boldsymbol{\beta}^{(k)}_{u}, and \boldsymbol{\xi}^{(k)}, imputed values of

\mathbf{C}^{(k)} are generated from the

corresponding Bernoulli distribution. Currently, the Bayesian mixture

model assumes that h(\cdot\,;\boldsymbol{\xi}) is constant

across all units.

The Bayesian adjustment is initialized using

adjMixBayes(), which optionally accepts customized prior

distributions and the current specifications of the prior distribution

for the different models is described in Appendix B:

adj_bayes <- adjMixBayes(

linked.data,

priors # Optional custom hyperparameters

)The model is then fitted using a standard wrapper, where the MCMC

iterations and computational cores can be controlled using the

control argument. In addition to GLMs, the package also

provides plsurvreg() for time-to-event outcomes. This

function extends the Bayesian mixture framework to survival data by

specifying p_m and p_u as parametric survival models. The

function call is:

plsurvreg(formula, dist = "weibull", adjustment, control, ...)The parameters formula and data specify the

survival regression model, where the response must be a

Surv() object with right-censoring. The dist

option defines the parametric form of the survival outcome models p_m and p_u,

with current choices including "weibull" and

"gamma". The parameter control is a list that

specifies the MCMC settings, including the number of iterations,

burn-in, random seed, and number of computational cores. These options

control posterior sampling and can be tuned to balance computational

cost with estimation accuracy. We note that the plcoxph()

function implements the semi-parametric Cox proportional hazards model,

and treats the baseline hazard non-parametrically. In contrast, the

plsurvreg() function uses a fully parametric survival model

when performing Bayesian inference.

Finally, to support multiple imputation, the package provides the

mi_with() function:

mi_with(object, data, formula, family)This function extracts samples of the latent match indicators from

the glmMixBayes or survMixBayes objects. Using

these samples, it repeatedly fits a user-specified regression model

(formula and family) on the subset of records

classified as correct matches for each MCMC draw. Estimates across

imputations are aggregated using standard combination rules for multiple

imputation (Little

& Rubin, 2002; Rubin,

1996).

4. Illustrations

We illustrate the implementation of the different post-linkage

adjustment methods and their inclusion of paradata available from the

linkage process. We simulate a linkage pipeline using the

RLdata10000 dataset from the RecordLinkage

package (Sariyar

& Borg, 2025).

A secondary analysis environment is generated with an approximate 30%

mismatch rate by constructing two separate datasets. Dataset A consists

of 1,000 unique records and contains the demographic and clinical

predictors: BMI, Age, and a binary

Treatment indicator. Dataset B contains the binary outcome

variable, Disease_Status. To construct these datasets, we

use the RLdata10000 data as identifiers of entities that

possess two distinct records, which often contain natural typographical

errors. We randomly selected 700 of these record pairs, allocating the

first instance to Dataset A and the corresponding error-prone second

instance to Dataset B. To complete the 1,000-record cohorts, the

remaining 300 records in Dataset A and 300 records in Dataset B were

sampled from mutually exclusive sets of identifiers representing unique,

unmatchable entities. This design guarantees 700 true matchable entities

across the files, systematically enforcing a mismatch rate of at least

30% when the files are linked as described below. Both datasets share a

set of error-prone quasi-identifiers used for the linkage process: first

name, last name, and date of birth. We assume that the linkage process

is strongly non-informative, so that the linkage errors are independent

of the variables used in the post-linkage analysis (Kamat & Gutman,

2026).

The two files are linked probabilistically with the

fastLink package that implements the Fellegi-Sunter model

(Fellegi & Sunter,

1969). To maintain an analytical cohort of n=1000 units, unlinked records from both

files are paired uniformly at random. Within this linked dataset, a

subset of records was designated as “safe matches” if both the first and

last names exhibit exact string agreement across the datasets.

The primary objective is to fit a logistic regression model to

estimate the probability of the outcome (Disease_Status)

given the covariates (BMI, Age, and

Treatment). Formally, the analysis model is given by:

\begin{aligned} \text{logit}(P(Y_i = 1 \mid \text{BMI}_i, \text{Age}_i, \text{Treatment}_i)) &= \beta_0 + \beta_{\text{BMI}}\text{BMI}_i \\ &\quad + \beta_{\text{Age}}\text{Age}_i + \beta_{\text{Treatment}}\text{Treatment}_i \end{aligned}

For comparability of effect sizes across the continuous and binary

predictors, both BMI and Age were standardized

to have a mean of zero and a standard deviation of one. The true

data-generating parameters are set to \beta_{0}=-1, \beta_{\text{BMI}}=1.2, \beta_{\text{Age}}=0.8, and \beta_{\text{Treatment}}=-1.5.

In a secondary analysis setting, the analyst has access to the analytical variables merged from both files, along with linkage paradata (e.g., blocking variables and continuous Jaro–Winkler string distances), but does not observe the latent true match indicator. Rather than using raw identifying strings, which are typically unavailable because of privacy constraints, the models rely on these distance metrics and safe match designations to assess linkage quality.

Table 2 illustrates the structure of the linked data,

dat.linked, available for the secondary analysis. While the

analyst observes the scientific variables (Disease_Status,

BMI, Age, Treatment) and the

linkage paradata (jw_fname, jw_lname,

safe_match), the latent true match indicator is absent. The

data contains a mix of exact matches where safe_match is

TRUE, probable matches with high string distances, and

false links characterized by near-zero Jaro-Winkler similarities.

Table 2: A sample of the linked dataset available for secondary analysis, containing scientific covariates and linkage paradata, but lacking true match status.

Disease_Status |

BMI |

Age |

Treatment |

jw_fname |

jw_lname |

safe_match |

|---|---|---|---|---|---|---|

| 0 | 0.777 | 1.320 | 0 | 0.000 | 0.550 | FALSE |

| 0 | 0.571 | 0.957 | 0 | 0.750 | 0.514 | FALSE |

| 0 | -0.145 | -0.036 | 1 | 1.000 | 0.978 | FALSE |

| 0 | 0.701 | -0.564 | 0 | 0.540 | 0.550 | FALSE |

| 0 | -1.346 | 0.174 | 1 | 0.971 | 1.000 | FALSE |

We demonstrate the performance of the different methods using the available paradata and compare them to cases where we know the truth or use naive methods.

4.1 The Benchmarks (Models 1–3)

The first three models represent standard approaches that do not

utilize postlink:

Oracle: The unobservable gold standard, logistic regression fit on the true, perfectly linked data.

Naive: A standard logistic regression fit on the probabilistically linked data that ignores the presence of false links.

Naive (Exact matches only): The analyst restricts the regression to only to links with the highest confidence (exact string matches on both first and last names), discarding the rest of the dataset.

4.2 Aggregate Information (Model 4)

If the analyst has access to block-level mismatch rates based on

clerical review, the adjELE() constructor can be utilized.

We define the blocks using the birth month (bm) variable.

We simulate an analyst reviewing a random audit sample of 20 records per

birth-month block.

R> adj_ele_audit <- adjELE(linked.data = dat.linked, m.rate = m.rate_vec,

+ blocks = ~ bm, audit.size = audit_sizes,

+ weight.matrix = "BLUE")

R> formula_sci <- Disease_Status ~ BMI + Age + Treatment

R> fit_ele_audit <- plglm(formula_sci, family = "binomial",

+ adjustment = adj_ele_audit)In practice, the choice of blocking variables for post-linkage adjustment should mimic the blocking algorithms used by the underlying record linkage algorithm, because mismatch rates tend to be more similar within these blocks.

4.3 Probabilistic Paradata (Models 5–7)

If continuous or categorical paradata from the linkage process is

retained, it can be passed into the adjMixture()

constructor. We demonstrate three progressively information-rich

applications of the EM mixture model. Model 5 relies on a known global

mismatch rate:

R> adj_em_rate <- adjMixture(linked.data = dat.linked,

+ m.formula = ~ 1,

+ m.rate = global_mismatch_rate)

R> fit_em_rate <- plglm(formula_sci, family = "binomial",

+ adjustment = adj_em_rate) Model 6 enhances Model 5 by incorporating a logical indicator for exact matches, allowing the algorithm to fix the match probability to 1 for highly confident records:

R> adj_em_safe <- adjMixture(linked.data = dat.linked,

+ m.formula = ~ 1,

+ m.rate = global_mismatch_rate,

+ safe.matches = dat.linked$safe_match_exact)

R> fit_em_safe <- plglm(formula_sci, family = "binomial",

+ adjustment = adj_em_safe)In Model 7, we drop the global rate constraint and incorporate the continuous Jaro-Winkler string distances for first and last names directly. This allows the mixture model to predict the match indicators (C_i) using the linkage paradata (\mathbf{Z}_i), which are the auxiliary covariates introduced in Equation 3.

4.4 Prior Knowledge (Model 8)

If the analyst has historical data or domain expertise regarding the

scientific parameters, the adjMixBayes() constructor allows

for the integration of this prior knowledge. In Model 5, the match rate

is set to a scalar. The Bayesian mixture framework accommodates

probability distributions that represent the uncertainty of the analyst

regarding the true match rate. In settings where relationship between

Y_{A} and \mathbf{X}_B is weak, it may be hard to

distinguish between true and false links without large number of units.

However, incorporating paradata in the form of prior distributions, such

as knowing the effect of age is positive and bounded or the approximate

error rate, can assist in the estimation process and result in more

reliable parameter estimates. The priors argument is a list

of prior distributions for model parameters, and it depends on the

family of distributions (See Appendix B).

In many record linkage applications one would expect that Y_{Ai} is independent or approximately

independent from \mathbf{X}_{Bi} among

false links (Guha

et al., 2022; Slawski et al.,

2025). This assumption may not be valid when the variables

used to create blocks are associated with Y_{Ai} and \mathbf{X}_{Bi} (Kamat et al., 2023). For this

simulation, we will maintain this independence assumption to demonstrate

the specification of prior distributions. Implementing this assumption

in the form of prior distribution assumes that a-priori the intercept

among mismatched links, intercept2, is centered at -1.28 and standard deviation of 3. The center

of the prior distribution is derived from the empirical log-odds of the

outcome prevalence in the linked dataset. The standard deviation of 3

result in relatively diffused prior distribution for the intercept of a

logistic regression model. To enforce independence between Y_{Ai} and \mathbf{X}_{Bi} among mismatched links, we

assumed that slope parameters, beta2, follow \mathcal{N}(0, 0.01), which reflects that the

coefficient is centered at zero with very small standard deviation. This

prior distribution requires significant input from the observed data to

deviate from 0. Lastly, to incorporate that 70% of the links are true

links, we assumed that the prior distribution for the marginal

proportion of true links, theta, follows a Beta

distribution with shape parameters 70 and 30. This implies that the mean

of the distribution is 0.7 and the standard deviation is 0.05.

4.5 Results and Discussion

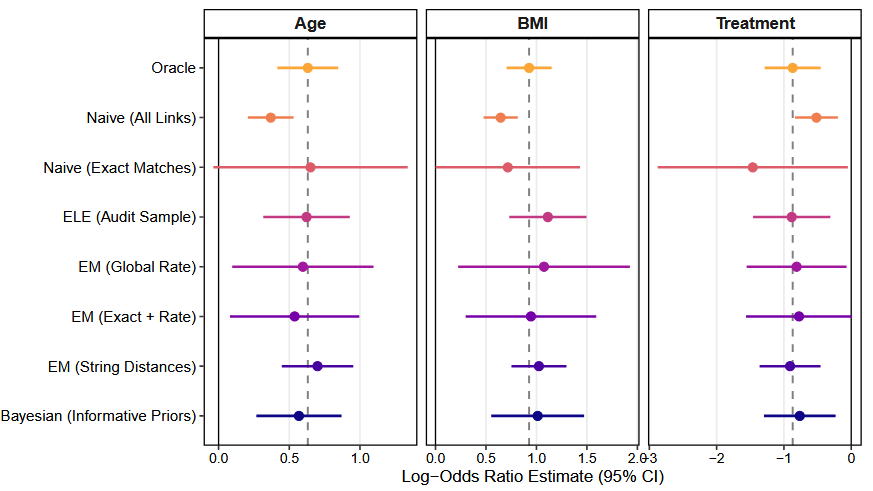

The coefficient estimates and 95% confidence intervals for all seven scenarios are detailed in Table 3. These results illustrate the potential biases introduced by linkage errors and the relative usage of different post-linkage adjustment strategies.

Ignoring the 30% mismatch rate (Model 2) results in estimates that are biased towards zero. For example, the estimate for \beta_{BMI} is attenuated by approximately 30% compared to the Oracle benchmark (from 0.927 by the Oracle down to 0.645 by the Naive), and its 95% confidence interval fails to include the true parameter. Relying on this unadjusted analysis would lead to underestimation of the relationship between the outcome and the covariate.

An alternative heuristic approach is to restrict the analysis to only high-confidence matches (Model 3). While this successfully eliminates the false links, it discards a significant portion of the dataset. By requiring exact name matches, the effective sample size is reduced from N=1000 to N\approx70, causing the standard error for the Treatment effect to more than triple (from 0.212 to 0.721). The confidence intervals are wider and the statistical power of the analysis is reduced. Moreover, when units with lower-confidence matches have different relationship between \mathbf{Y}_A and \mathbf{X}_B than high-confidence matches, bias may be introduced.

The adjustment methods implemented in postlink mitigate

these limitations to varying degrees. The ELE approach (Model 4) shifts

the estimates toward the true parameters’ values. Because the

audit.size argument was supplied, the standard errors

increase to account for the sampling variance inherent in the clerical

review, providing more appropriately calibrated inference. The EM

Mixture model using continuous Jaro-Winkler string distances (Model 7)

demonstrates favorable performance. By incorporating continuous

paradata, the algorithm assigns probabilistic weights to the reliability

of individual records, recovering point estimates comparable to the

Oracle model without the large variance inflation observed in the exact

matches only approach. We note, however, that the simulated separation

between the high string distances of true matches and the near-zero

distances of forced random mismatches creates a comparatively

straightforward classification task. In applied settings where false

links share higher string similarity (e.g., matching ‘John Smith’ to

‘Jon Smith’ erroneously), the resulting overlap of the distributions

p_m and p_u would naturally increase the standard

errors of the estimated model parameters. The point estimates of the

Bayesian model are comparable to Model 5. However, because the prior

distributions allow for more variability in the mismatch rate and the

estimates of regression parameters among non-links leads to larger

standard errors, but still smaller than the high confidence matches

analysis (Model 3).

Table 3: Logistic regression estimates and standard errors (SE) from the benchmark models and post-linkage adjustment methods.

| Model | Est. (Intercept) | SE (Intercept) | Est. (BMI) | SE (BMI) | Est. (Age) | SE (Age) | Est. (Treatment) | SE (Treatment) |

|---|---|---|---|---|---|---|---|---|

| 1. Oracle | -1.243 | 0.139 | 0.927 | 0.114 | 0.631 | 0.110 | -0.870 | 0.212 |

| 2. Naive (All Links) | -1.176 | 0.109 | 0.645 | 0.086 | 0.369 | 0.083 | -0.517 | 0.163 |

| 3. Naive (Exact Matches) | -0.791 | 0.376 | 0.716 | 0.365 | 0.650 | 0.351 | -1.463 | 0.721 |

| 4. ELE (Audit Sample) | -1.233 | 0.164 | 1.113 | 0.195 | 0.622 | 0.156 | -0.884 | 0.293 |

| 5. EM (Global Rate) | -1.231 | 0.199 | 1.075 | 0.434 | 0.596 | 0.255 | -0.811 | 0.379 |

| 6. EM (Exact + Rate) | -1.184 | 0.174 | 0.945 | 0.330 | 0.538 | 0.233 | -0.776 | 0.402 |

| 7. EM (String Distances) | -1.240 | 0.157 | 1.025 | 0.139 | 0.700 | 0.129 | -0.909 | 0.231 |

| 8. Bayesian (Informative) | -1.099 | 0.419 | 1.029 | 0.251 | 0.573 | 0.162 | -0.782 | 0.282 |

4.6 Decoupling Linkage and Analysis via Multiple Imputation

While the adjMixBayes() constructor performs joint

estimation of the linkage and outcome models, MCMC sampling is

computationally intensive. In practice, analysts frequently conduct

exploratory model building, assessing various interactions, polynomials,

or covariate combinations. Repeatedly fitting the joint Bayesian model

for each exploratory iteration introduces a computational

bottleneck.

The postlink package addresses this computational

complexity by using multiple imputation (Gutman et al., 2016), which is

implemented with the mi_with() generic function. Because

the Bayesian mixture model returns posterior draws of the latent match

status for every record, each draw effectively generates one completed

dataset. The mi_with() function extracts these latent

assignments, fits a user-specified regression model on the subset of

records classified as correct matches for each MCMC draw, and aggregates

the results using common combination rules for multiple imputation (Rubin, 1987). This

allows the analyst to run the MCMC procedure once and subsequently

explore alternative scientific models more efficiently. For example, if

the analyst is only interested in the marginal effect of

Treatment, they can pass the updated formula to the

pre-computed adjustment object:

R> formula_interaction <- Disease_Status ~ Treatment

R> pooled_mi_fit <- mi_with(object = fit_bayes_strong,

+ data = dat.linked,

+ formula = formula_interaction,

+ family = binomial())

R> print(pooled_mi_fit, digits = 3)

#> Pooled regression results across posterior match classifications:

#> Retained imputations (m): 9000

#>

#> Estimate Std.Error CI.lwr CI.upr df

#> (Intercept) -0.868 0.288 -1.432 -0.304 13017.312

#> Treatment -0.629 0.227 -1.074 -0.184 82594.793As detailed in the output, the marginal term for

Treatment is estimated to be significantly different from

zero at the 5% nominal level (95% CI: -1.067, -0.183), which is

consistent with the underlying data-generating process. This model

exploration utilized 1,000 posterior draws as imputed datasets,

demonstrating how linkage error estimation can be decoupled from

downstream scientific modeling. When utilizing multiple imputation one

should attempt to avoid uncongenial models (Meng, 1994). Thus, it is

advisable to include many relationships of substantive interest when

classifying between true and false links, so that the analysis model is

more restrictive than the imputation model (Kamat & Gutman, 2026; Meng, 1994).

Figure 2: Correction for Attenuation Bias from Linkage Errors in Logistic Regression. The dashed line represents the true Oracle estimates.

5. Conclusion

Record linkage is widely used to combine information of interest

scattered across multiple datasets. Datasets that were created using

linkage algorithms that are based on quasi-identifiers, often suffer

from linkage errors. These datasets are frequently analyzed without

regard for these linkage errors. The lack of easy-to-use software

implementing existing methods adjusting for such errors is likely a

major contributing factor. This lack is in contrast to the availability

of software for performing linkage. In this paper, we introduce the

postlink package, which equips researchers with three

state-of-the-art methods for post-linkage regression analysis through an

interface that mimics standard R modeling functions (e.g.,

stats::glm(), survival::coxph()). Our

implementations offer a variety of ways to incorporate information about

linkage quality in secondary analysis settings, which we expect to be

useful for practitioners working with linked data sets. The current

version of the package leaves room for various extensions, including

additional types of post-linkage analysis models, support for missed

matches (i.e., records that could not be linked) in addition to

mismatches, and integration with record linkage software.

Computational Details

The results and illustrations in this article were obtained using R

4.3.2 and the postlink package version 0.1.0. R itself and

all standard dependent packages, including survival for

time-to-event outcomes, nleqslv for solving estimating

equations, and fastLink for the probabilistic record

linkage, are available from the Comprehensive R Archive Network (CRAN)

at https://CRAN.R-project.org/. The Bayesian mixture

modeling routines in postlink utilize Hamiltonian Monte

Carlo sampling and require a functional C++ toolchain. These routines

depend on the rstan and rstantools packages,

which are also available from CRAN.

The postlink package and datasets used for the

application are open-source and publicly available. The development

version can be accessed and installed from GitHub at https://github.com/postlink-group/postlink. To ensure

exact reproducibility of the Bayesian data augmentation and the

Expectation-Maximization algorithms, specific random seeds were set

prior to model fitting. Full replication scripts for all illustrations

and simulations presented in this article are provided in the

supplementary materials.

Acknowledgments

Priyanjali Bukke, Jiahao Cui, Roee Gutman, and Martin Slawski were supported by NSF grant # 2411270. Bukke and Slawski were additionally supported by NSF grant # 2120318.

Appendix A: Computational and variance estimation details for the ELE model

A.1 Computation of expected design matrices

To solve the adjusted estimating equations, we compute the product of the expected linkage matrix E_q and the block-level design matrix \mathbf{X}_{Bq} (or a function of it, denoted by M_q). Constructing the n_q \times n_q matrix E_q and performing standard matrix multiplication requires \mathcal{O}(n_q^2 d) floating-point operations (flops) per block, which is computationally prohibitive for large datasets.

The postlink package circumvents this by exploiting the

structural properties of the ELE model. Let \alpha_q = 1 - \lambda_q represent the

mismatch rate. The product E_q M_q can

be analytically rewritten as a linear combination of the observed values

and their block-specific column means:

E_q M_q = c_{1q} M_q + c_{0q} \bar{M}_q

where \bar{M}_q represents the

column means of M_q, and the scalars

are defined as c_{1q} = 1 - \alpha_q -

\alpha_q / (n_q - 1) and c_{0q} =

\alpha_q \frac{n_q}{n_q - 1}. This formulation reduces the

computational complexity to \mathcal{O}(n_q

d). The postlink implementation applies this

optimization globally across the internal glmELE() and

coxphELE() routines, utilizing vectorized aggregation

functions (e.g., rowsum()) to ensure scalable model fitting

and risk-set evaluation.

A.2 Variance estimation and audit sample uncertainty

The variance of the ELE estimators is computed using a sandwich estimator, \widehat{\text{Var}}(\widehat{\boldsymbol{\beta}}) = J^{-1} V_H (J^{-1})^\top, where J is the Jacobian matrix of the estimating equations evaluated at \widehat{\boldsymbol{\beta}}. The variance of the estimating functions, V_H, is decomposed as V_H = V_1 + V_2.

The term V_2 represents the

empirical covariance of the estimating functions assuming the mismatch

rates \lambda_q are fixed and known.

When the mismatch rates are estimated via a simple random audit sample

of size m_q drawn from the n_q records in block q (supplied via the audit.size

argument), the package computes V_1 to

account for this additional source of uncertainty.

The implementation applies a finite population correction (FPC) to

accurately reflect the sampling fraction:

V_1 = \sum_{q=1}^Q \left( \frac{1}{m_q} - \frac{1}{n_q} \right) \left(

\frac{m_q}{m_q - 1} \right) \frac{\alpha_q}{\lambda_q^3} U_q U_q^\top

where U_q is the block-specific

sum of the weighted residuals. This accounting of audit uncertainty

ensures that the standard errors returned by standard post-estimation

generics, such as confint() and vcov(),

provide valid statistical inference even when linkage quality is

estimated from small clerical reviews.

Appendix B: Default Prior Distributions for Each Family of Distributions

Bayesian adjustment methods require the specification of the prior

distribution. The specifications of all the prior distributions follow

the Stan programming language syntax (Stan Development Team, 2024). The prior

distributions include independent prior distributions for the intercept

among true links, intercept1, and the intercept among

non-links intercept2. To reduce the burden on analysts, we

assume the same independent prior distribution for all the slope

coefficients among true links, beta1, and the same

independent prior distribution among all false links,

beta2. All of the models support a prior distribution on

the marginal probability of being a true link, theta. The

other prior distributions are specific for each of the models. The prior

for GLM regressions are:

"gaussian" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,5)",

sigma1 = "cauchy(0,2.5)",

beta2 = "normal(0,5)",

sigma2 = "cauchy(0,2.5)",

theta = "beta(1,1)"

)

"poisson" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,5)",

beta2 = "normal(0,5)",

theta = "beta(1,1)"

)

"binomial" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,2.5)",

beta2 = "normal(0,5)",

theta = "beta(1,1)"

)

"gamma" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,5)",

beta2 = "normal(0,5)",

phi1 = "gamma(2,0.1)",

phi2 = "gamma(2,0.1)",

theta = "beta(1,1)"

)The prior distributions for the parametric time-to-event models:

"gamma" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,5)",

beta2 = "normal(0,5)",

phi1 = "exponential(1)",

phi2 = "exponential(1)",

theta = "beta(1,1)"

)

"weibull" = list(

intercept1 = "normal(0,10)",

intercept2 = "normal(0,10)",

beta1 = "normal(0,2)",

beta2 = "normal(0,2)",

shape1 = "gamma(2,1)",

shape2 = "gamma(2,1)",

scale1 = "gamma(2,1)",

scale2 = "gamma(2,1)",

theta = "beta(1,1)"

)